Facing foreclosure can feel overwhelming, especially when missed mortgage payments continue piling up and foreclosure notices begin arriving in the mail. Many Washington homeowners dealing with financial hardship, job loss, divorce, medical debt, inherited property issues, or costly home repairs start asking the same urgent question: can bankruptcy stop foreclosure in Washington?

The answer is yes — in many situations, bankruptcy may temporarily stop foreclosure proceedings. However, the type of bankruptcy filed, the timing of the filing, and the homeowner’s financial situation all play important roles in determining what happens next.

Although bankruptcy may provide temporary foreclosure protection through an automatic stay, it is not always the only option available. Some homeowners choose loan modification, repayment plans, short sales, or selling the property before foreclosure becomes final. Others decide that a fast as-is home sale provides a simpler and less stressful solution.

At We Buy House As Is, we work with homeowners throughout Washington who are facing foreclosure deadlines and need fast options before their homes reach trustee sale. Understanding how bankruptcy and foreclosure work together may help you make more informed financial decisions before the situation becomes more serious.

How Foreclosure Works in Washington

Washington primarily uses a non-judicial foreclosure process, meaning lenders can foreclose without going through court. Because of this, foreclosure timelines can move relatively quickly once homeowners fall behind on mortgage payments.

The foreclosure process usually begins after several missed payments and may include:

- late notices

- collection calls

- Notice of Default

- Notice of Trustee Sale

- foreclosure auction scheduling

Many homeowners begin researching Washington foreclosure timelines as soon as foreclosure notices arrive because they want to understand how much time they still have before losing the property.

If the mortgage debt remains unresolved, the property may eventually be sold at foreclosure auction, also called a trustee sale.

Homeowners often review what happens after a Notice of Default before deciding whether bankruptcy or another foreclosure alternative makes the most sense financially.

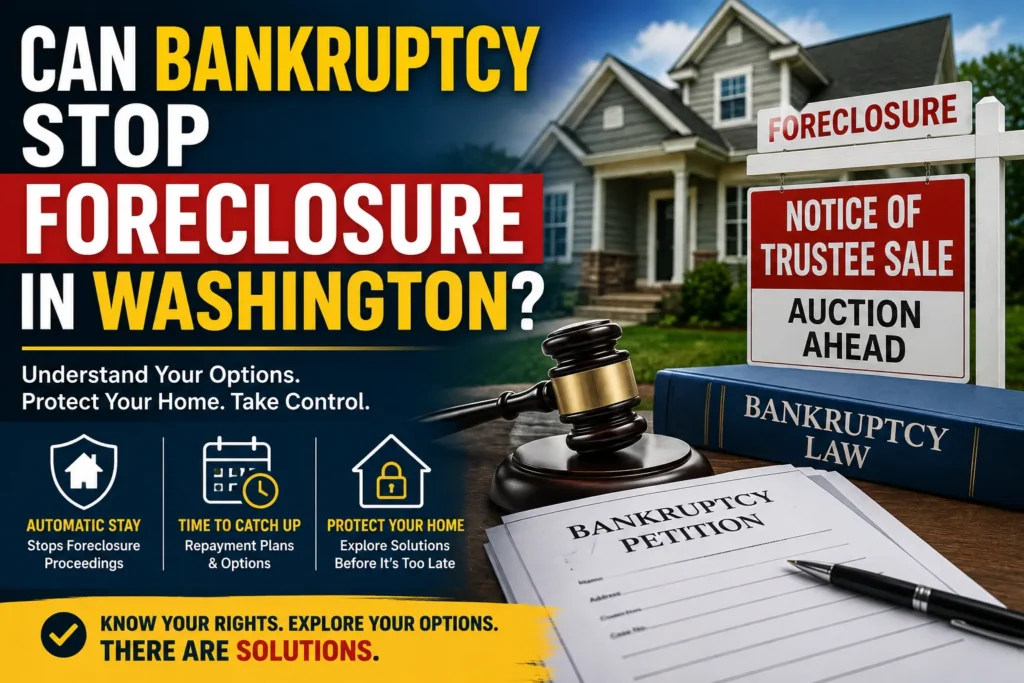

Can Bankruptcy Stop Foreclosure in Washington?

Yes. Filing bankruptcy may temporarily stop foreclosure proceedings in Washington through a legal protection known as an automatic stay.

An automatic stay immediately pauses many debt collection activities, including:

- foreclosure proceedings

- collection calls

- wage garnishments

- creditor lawsuits

- trustee sale activity

This temporary pause may give homeowners time to:

- reorganize finances

- negotiate with lenders

- explore foreclosure alternatives

- sell the property

- create repayment plans

However, bankruptcy does not always permanently stop foreclosure. In many cases, it delays foreclosure proceedings while homeowners evaluate their next steps.

The earlier homeowners act, the more foreclosure protection options may still be available.

What Is an Automatic Stay?

An automatic stay is one of the most important legal protections created when bankruptcy is filed.

Once bankruptcy paperwork is officially submitted:

- foreclosure proceedings may pause

- trustee sales may be delayed

- lenders may temporarily stop collection actions

- creditors must follow bankruptcy court rules

For homeowners facing urgent foreclosure deadlines, the automatic stay may provide valuable additional time.

Many distressed homeowners researching bankruptcy also begin exploring ways to stop a trustee sale before foreclosure auctions occur.

Although the automatic stay can temporarily stop foreclosure, lenders may eventually ask the bankruptcy court for permission to continue foreclosure proceedings depending on the homeowner’s financial situation.

Chapter 7 vs Chapter 13 Bankruptcy for Foreclosure

The two most common forms of personal bankruptcy used during foreclosure are Chapter 7 and Chapter 13 bankruptcy.

Each affects foreclosure differently.

Chapter 7 Bankruptcy and Foreclosure

Chapter 7 bankruptcy is sometimes called liquidation bankruptcy.

This type of bankruptcy may:

- temporarily stop foreclosure

- eliminate certain unsecured debts

- provide short-term financial relief

However, Chapter 7 does not usually provide a long-term solution for homeowners who cannot catch up on mortgage payments.

In many cases:

- the automatic stay temporarily pauses foreclosure

- the lender eventually resumes foreclosure proceedings

- the trustee sale may continue later

Because of this, Chapter 7 is often viewed as a temporary foreclosure delay rather than a permanent foreclosure solution.

Homeowners dealing with serious financial hardship sometimes compare bankruptcy with foreclosure vs short sale options before deciding how to move forward.

Chapter 13 Bankruptcy and Foreclosure

Chapter 13 bankruptcy works differently because it creates a structured repayment plan.

Instead of immediately liquidating debts, Chapter 13 may allow homeowners to:

- catch up on missed mortgage payments

- reorganize debt

- make monthly repayment plans

- keep the property longer

For some homeowners, Chapter 13 provides a more effective foreclosure prevention strategy because it offers additional time to repay mortgage arrears.

However, homeowners must still:

- make ongoing mortgage payments

- follow court-approved repayment plans

- maintain stable income

Because bankruptcy courts closely monitor Chapter 13 repayment plans, homeowners should fully understand their financial obligations before proceeding.

Can Bankruptcy Stop a Trustee Sale?

In many situations, yes.

If bankruptcy is filed before the foreclosure auction occurs, the automatic stay may temporarily stop or delay the trustee sale.

Timing is extremely important.

Once the trustee sale is completed:

- ownership may transfer away from the homeowner

- foreclosure becomes much harder to reverse

- legal options may become limited

Because Washington foreclosure timelines can move quickly, homeowners should avoid waiting until the final moment before exploring bankruptcy or other foreclosure alternatives.

Many distressed homeowners also compare bankruptcy with selling a home during foreclosure because selling before auction may help preserve remaining home equity.

Can You Keep Your House After Filing Bankruptcy?

Possibly. Whether homeowners can keep their homes after bankruptcy depends on several factors, including:

- income

- mortgage balance

- lender cooperation

- repayment ability

- type of bankruptcy

- home equity

- ongoing financial hardship

Some homeowners successfully use Chapter 13 bankruptcy to catch up on missed payments over time.

Others eventually realize that keeping the property is no longer financially realistic and choose to sell instead.

Many homeowners facing foreclosure deadlines compare selling to a cash buyer vs using an agent because traditional home sales may take too long during foreclosure proceedings.

Alternatives to Bankruptcy Before Foreclosure

Bankruptcy is not always the only foreclosure prevention strategy available.

Depending on the situation, homeowners may also consider:

- loan modification

- repayment plans

- refinancing

- short sales

- forbearance agreements

- selling the property

Some homeowners decide that avoiding bankruptcy entirely is the better long-term financial decision.

Others choose to sell quickly before foreclosure becomes final.

Many distressed homeowners throughout Washington begin researching foreclosure prevention options as soon as mortgage delinquency becomes serious.

Can You Sell Your House During Bankruptcy?

Yes. In many situations, homeowners may still sell their homes during bankruptcy proceedings.

However:

- court approval may sometimes be required

- lender communication remains important

- repayment obligations may affect proceeds

Selling the property may help homeowners:

- resolve mortgage debt

- avoid foreclosure auctions

- reduce financial stress

- simplify bankruptcy proceedings

For homeowners already dealing with costly repairs, selling as-is may provide additional flexibility.

Many distressed homeowners choose selling a house as-is because they cannot afford renovations before foreclosure deadlines arrive.

How Cash Home Buyers Help During Foreclosure

Cash home buyers frequently work with homeowners facing:

- foreclosure

- bankruptcy

- inherited property issues

- divorce

- costly repairs

- tenant damage

- delinquent taxes

- urgent relocation

Because cash transactions avoid financing delays, they often close faster than traditional home sales.

At We Buy House As Is, we help homeowners sell properties as-is without:

- realtor commissions

- repairs

- staging

- cleaning

- lengthy listing timelines

Many homeowners choose cash sales because they provide:

- flexible timelines

- simplified paperwork

- faster closings

- fewer contingencies

- reduced stress during foreclosure

If speed matters, our article explaining how all-cash home sales work explains why cash transactions often close faster than traditional financed sales.

Homeowners also frequently research how to choose a reputable cash buyer before accepting a cash offer.

Common Reasons Homeowners Consider Bankruptcy During Foreclosure

Job Loss or Reduced Income

Unexpected income loss is one of the most common reasons homeowners fall behind on mortgage payments.

Medical Bills

Medical debt and rising healthcare expenses can quickly create financial hardship for families already managing mortgage obligations.

Divorce

Divorce often creates financial instability and may require selling the family home quickly. Homeowners dealing with both foreclosure and divorce frequently explore selling a home during divorce to reduce financial pressure.

Inherited Property Problems

Inherited homes sometimes come with:

- mortgage debt

- unpaid taxes

- deferred maintenance

- probate complications

Many heirs research selling an inherited house fast when ownership costs become overwhelming.

Costly Repairs

Major repair issues involving:

- roofing

- plumbing

- mold

- structural damage

- fire damage

can create additional financial stress during foreclosure proceedings.

Homeowners facing serious condition problems often research:

before deciding how to sell.

Tenant Problems

Landlords dealing with severe tenant damage or unpaid rent may also struggle to maintain mortgage payments.

Washington property owners frequently explore selling a house trashed by tenants when repair costs become financially overwhelming.

Frequently Asked Questions

Can bankruptcy stop foreclosure in Washington?

Yes. Filing bankruptcy may temporarily stop foreclosure proceedings through an automatic stay.

Does Chapter 13 stop foreclosure?

In many situations, Chapter 13 may help homeowners catch up on missed payments through a repayment plan.

Can bankruptcy stop a trustee sale?

Yes. If bankruptcy is filed before the foreclosure auction occurs, the automatic stay may temporarily delay the trustee sale.

Can I keep my house after bankruptcy?

Possibly. It depends on your repayment ability, income, home equity, and bankruptcy type.

Can I sell my house during bankruptcy?

Yes. Many homeowners sell their properties during bankruptcy proceedings, although court approval may sometimes apply.

Final Thoughts

Bankruptcy may help stop foreclosure in Washington depending on your financial situation and how quickly you act. Whether you pursue Chapter 7, Chapter 13, loan modification, repayment plans, or selling the property before foreclosure auction, understanding your options early may help protect your home equity and reduce long-term financial damage.

However, bankruptcy is not always the only foreclosure solution available. Many distressed homeowners throughout Washington eventually decide that selling the property provides a simpler and less stressful path forward before foreclosure becomes final.

At We Buy House As Is, we help homeowners facing foreclosure, bankruptcy, and financial hardship with fast as-is home sales, fair cash offers, and flexible closing timelines.

If you need to sell your house quickly before foreclosure becomes final, contact We Buy House As Is today for a free no-obligation cash offer and explore your options before time runs out.