Falling behind on mortgage payments can be one of the most stressful experiences a homeowner faces. Many Washington homeowners dealing with financial hardship, job loss, divorce, medical expenses, or rising living costs often wonder how long the foreclosure process takes and whether there is still time to save their home or sell the property before foreclosure is finalized.

Understanding the Washington foreclosure timeline is extremely important because acting early may help you avoid long-term financial consequences. In many cases, homeowners still have options even after receiving foreclosure notices from their lender.

Washington primarily uses a non-judicial foreclosure process, which means lenders can foreclose on a property without going through court. Because the process can move quickly, homeowners facing missed mortgage payments should understand the timeline, legal notices, and foreclosure alternatives available to them.

In this guide, we’ll explain how foreclosure works in Washington State, what happens after missed payments, how long foreclosure usually takes, and how homeowners may be able to stop foreclosure before a trustee sale occurs.

How the Foreclosure Process Works in Washington State

Washington State primarily follows a non-judicial foreclosure system under a deed of trust. This means the foreclosure process is handled outside the courtroom by a trustee rather than through a judge.

When homeowners stop making mortgage payments, the mortgage lender may begin foreclosure proceedings to recover the unpaid loan balance. The lender typically works with a mortgage servicer and trustee throughout the process.

Unlike judicial foreclosure states, Washington’s non-judicial foreclosure timeline can move relatively fast once formal notices begin.

Common reasons Washington homeowners face foreclosure include:

- job loss

- financial hardship

- divorce

- medical debt

- rising mortgage payments

- inherited property issues

- expensive home repairs

- tenant problems

- bankruptcy complications

Many distressed homeowners begin searching for foreclosure help after receiving late notices or a Notice of Default.

If you are already behind on payments, it’s important to understand the steps ahead and explore foreclosure alternatives before the foreclosure auction date arrives.

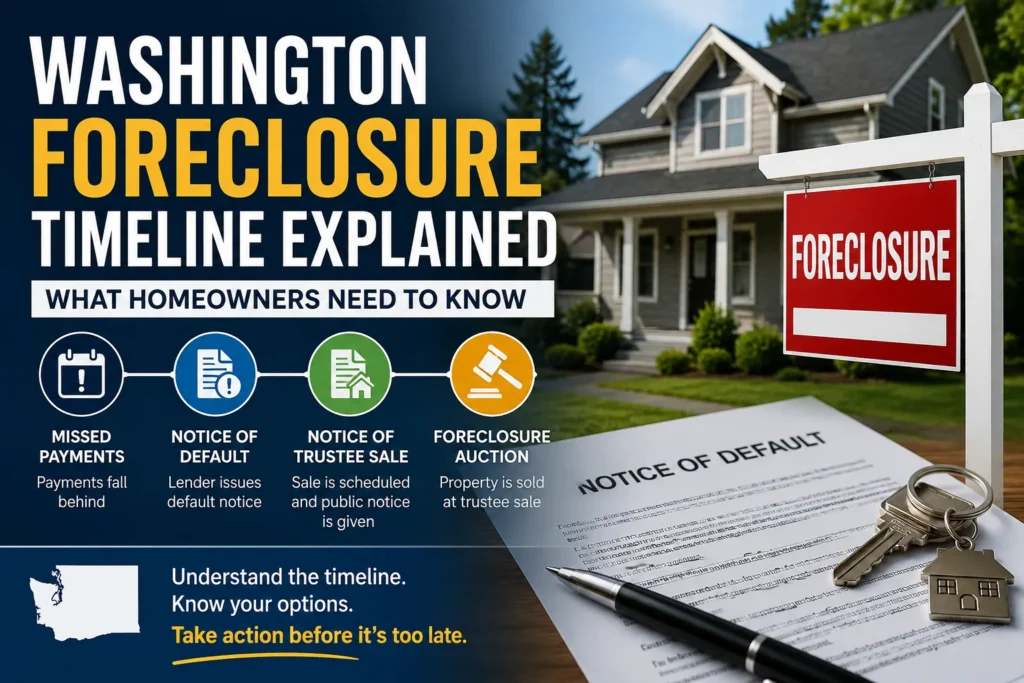

Step-by-Step Washington Foreclosure Timeline

Step 1: Missed Mortgage Payments

The foreclosure timeline usually begins after several missed mortgage payments.

Most lenders will first attempt to contact the homeowner regarding the delinquent mortgage balance. During this stage, homeowners may receive:

- late payment notices

- collection calls

- lender warnings

- default letters

The exact timing depends on the lender, but foreclosure proceedings often begin after 90 to 120 days of missed payments.

At this early stage, homeowners still have the most flexibility. Some options may include:

- repayment plans

- loan modification

- refinancing

- reinstatement agreements

- selling the property

- bankruptcy protection

Many Washington homeowners also begin exploring ways to sell their house fast before foreclosure becomes more serious.

Step 2: Notice of Default

If the missed mortgage payments are not resolved, the lender may issue a Notice of Default.

A Notice of Default is an official legal document informing the homeowner that the mortgage is seriously delinquent and foreclosure proceedings may continue if the balance is not brought current.

This stage is commonly referred to as pre-foreclosure.

The Notice of Default typically includes:

- total delinquent amount owed

- late fees and penalties

- reinstatement requirements

- timeline for resolving the default

- lender contact information

Receiving a Notice of Default can feel overwhelming, but homeowners still usually have time to take action.

Common foreclosure prevention strategies during this stage include:

- selling the home quickly

- negotiating with the lender

- seeking foreclosure mediation

- applying for hardship assistance

- working with cash home buyers

If you are unsure whether selling or working with a cash buyer is the right option, this guide compares common approaches.

Step 3: Notice of Trustee Sale

If the default remains unresolved, the lender may move forward with a Notice of Trustee Sale.

This notice formally schedules the foreclosure auction date and provides public notice that the property may soon be sold.

Under Washington foreclosure laws, homeowners generally receive advance notice before the trustee sale occurs.

The Notice of Trustee Sale may include:

- foreclosure sale date

- property information

- lender details

- auction location

- reinstatement deadlines

At this stage, homeowners often begin urgently searching:

- how to stop foreclosure in washington

- can i sell my house before foreclosure

- cash buyers foreclosure washington

- sell house fast before trustee sale

Even after a Notice of Trustee Sale has been issued, many homeowners can still sell the property before the foreclosure auction occurs.

For homeowners looking for foreclosure alternatives, our guide on avoiding foreclosure explains additional solutions:

Step 4: Foreclosure Auction / Trustee Sale

The trustee sale is the final stage of the foreclosure process. During the foreclosure auction, the property may be sold to:

- investors

- third-party buyers

- the mortgage lender

Once the trustee sale is completed, ownership transfers away from the homeowner.

At this point:

- the foreclosure becomes part of the homeowner’s financial history

- credit damage may occur

- eviction proceedings may eventually follow

Because of these risks, many distressed homeowners attempt to sell their house before the foreclosure auction date arrives.

Homeowners dealing with foreclosure and property damage often choose to sell as-is rather than invest in repairs.

How Long Does Foreclosure Take in Washington?

The Washington foreclosure timeline varies depending on:

- lender actions

- homeowner response

- mediation efforts

- bankruptcy filings

- repayment negotiations

However, the process often takes several months from the first missed payment to the foreclosure auction.

A simplified timeline may look like this:

| Stage | Approximate Timeline |

|---|---|

| Missed Payments Begin | Month 1 |

| Notice of Default | Month 3–4 |

| Notice of Trustee Sale | Month 4–5 |

| Trustee Sale / Auction | Month 6+ |

Because timelines can move quickly, acting early is critical.

Homeowners facing financial hardship should avoid waiting until the final weeks before the trustee sale to explore options.

Can You Sell Your House Before Foreclosure in Washington?

Yes, many Washington homeowners successfully sell their homes before foreclosure is finalized.

Selling during pre-foreclosure may help homeowners:

- avoid foreclosure on credit reports

- preserve remaining home equity

- reduce financial stress

- avoid lengthy legal complications

- move on faster financially

Homeowners often choose fast cash sales because traditional listings may take too long during foreclosure situations.

Benefits of selling to a cash buyer may include:

- fast closings

- no repairs required

- no realtor commissions

- flexible closing dates

- simplified paperwork

- fewer financing delays

Can Cash Buyers Help Stop Foreclosure?

In many situations, yes.

Cash home buyers frequently work with distressed homeowners facing:

- foreclosure

- bankruptcy

- inherited property issues

- delinquent taxes

- major repairs

- vacant homes

- tenant damage

Because cash sales often close faster than traditional home sales, they may help homeowners complete the transaction before the foreclosure auction occurs.

Washington homeowners often search for:

- we buy houses foreclosure washington

- cash buyers foreclosure help

- sell house quickly before foreclosure

- urgent home sale solutions

Foreclosure Alternatives for Washington Homeowners

Foreclosure is not always the only option available. Depending on your financial situation, alternatives may include:

- loan modification

- repayment plans

- refinancing

- forbearance

- bankruptcy

- short sale

- selling the home

Some homeowners also consider selling inherited or distressed properties during financial hardship.

Common Reasons Washington Homeowners Face Foreclosure

Foreclosure can happen to homeowners in all financial situations. Some of the most common causes include:

Job Loss or Reduced Income

Unexpected income loss is one of the most common reasons homeowners fall behind on mortgage payments. Rising expenses and economic uncertainty can quickly create financial hardship.

Divorce

Divorce often creates financial instability and may require selling the family home quickly to divide assets or reduce expenses. If you are navigating both divorce and mortgage concerns, our article on selling a home during divorce explains several important considerations.

Costly Repairs

Major repair costs involving roofing, plumbing, mold, fire damage, or structural issues can become financially overwhelming for homeowners already struggling with mortgage payments.

Inherited Property Problems

Inherited homes sometimes come with unpaid taxes, mortgage debt, deferred maintenance, or probate complications. If you recently inherited a property, our guide on selling an inherited house fast may help explain the process.

Tenant Issues

Rental property owners may face tenant damage, unpaid rent, or eviction complications.

Areas We Help Throughout Washington

We help homeowners throughout Washington State, including Seattle, Tacoma, Bellevue, Everett, Spokane, Kent, Olympia, Redmond, Kirkland, Renton, and surrounding communities.

Whether you are facing foreclosure near downtown Seattle, Tacoma’s waterfront, or suburban communities throughout King County and Snohomish County, there may still be options available before the foreclosure auction occurs.

Frequently Asked Questions

How many missed payments before foreclosure in Washington?

Most lenders begin foreclosure proceedings after several missed mortgage payments, often around 90 to 120 days delinquent.

Can I stop foreclosure after receiving a Notice of Default?

Possibly. Homeowners may still have options such as reinstatement, loan modification, bankruptcy, or selling the property.

Can I sell my house before the trustee sale?

Yes. Many homeowners successfully complete a sale before the foreclosure auction date.

Will foreclosure hurt my credit?

Yes. Foreclosure can significantly impact your credit score and remain on your credit history for years.

Can I sell a house with repairs needed?

Yes. Many cash home buyers purchase distressed properties as-is.

Final Thoughts

Facing foreclosure can be stressful, but understanding the Washington foreclosure timeline gives homeowners a better chance to act before the situation becomes more serious. Although foreclosure in Washington can move quickly, many homeowners still have opportunities to negotiate with lenders, explore foreclosure alternatives, or sell the property before the trustee sale occurs.

Whether you are dealing with missed mortgage payments, financial hardship, divorce, inherited property issues, or costly repairs, taking action early may help protect your remaining home equity and reduce long-term financial damage. Many distressed homeowners throughout Washington choose We Buy House As Is because we help simplify the process with fast, as-is home sales and flexible closing timelines.

If you need to sell your house quickly before foreclosure, We Buy House As Is can help you explore your options and move forward with greater confidence before time runs out.